I would think that is where you want to be. My wife and I are about 80-85% mutual funds for our retirement. Our financial adviser thinks that is fantastic.Sounds like it would be best to just stick with my current strategy. The only thing that concerns me is that probably 80% of my net worth is in retirement/savings accounts but I guess that's life.

No forums found...

Site Related

Iowa State

College Sports

General - Non ISU

CF Archive

Install the app

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

Mortgage/Retirement question

- Thread starter pfgemployee

- Start date

No forums found...

Site Related

Iowa State

College Sports

General - Non ISU

CF Archive

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Inflation is currently higher than your mortgage rate. I'd keep investing in low cost index funds and make those cheap mortgage payments for the next decade and be debt free after that.

Also, The new tax law caps mortgage interest deductions on $750,000 I believe.

Also, The new tax law caps mortgage interest deductions on $750,000 I believe.

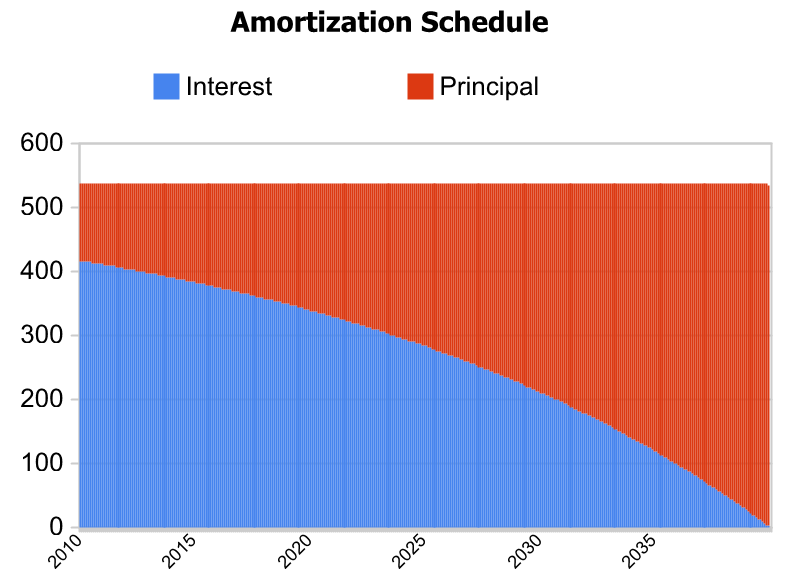

Run a quick amortization chart on your mortgage. On a 15 year note the portion of your payment allocated to interest at this point would be about 40% lesser than when it originated, or 50% less on a 30 year. As mentioned previously your effective rate at this point is actually less than 2.875, I'd stick with the 401k.

D

Deleted member 8507

Guest

Edward Jones is paying a pretty good CD rateThere is nothing that is guaranteeing that rate right now. Maybe an internet bank 60 month cd or special cd and you’d probably have to drop 100k minimum in it to get there.

Edward Jones is paying a pretty good CD rate

View attachment 56779

Very nice rates. Still wouldn’t recommend having that money locked up like that.

Very nice rates. Still wouldn’t recommend having that money locked up like that.

That’s why I bury my money in a hole in the backyard.

Great minds think alike. I was going to call it free money in my reply but held off. I am a big fan of free money. Those opportunities don't come around that often.I'd pump the 401k; that mortgage rate is pretty cheap and the owner match is free money.

Just to be clear, I was thinking about lowering the amount that I was putting in my 401k not my Roth 401k. My employer matches 6% on either as long as you do 6%.

Here is the scenario

Late 40's

We have about 6x our salary's in retirement funds with about 1/3 of that being in post tax accounts.

Currently do 6% in 401k and 14% in Roth 401k + employer match of 6%. We also have 1/3 years salary in emergency fund. No other debt besides mortgage.

Mortgage has 9 years left at 2.875%

Should I take the 6% that I'm putting towards my 401k and apply it towards the mortgage, which would cut 27 months off the payoff date?

2.8% money is really cheap money. If anything, just double your principal payment. Do the math on how much interest you'll be on the hook for - guessing it's a drop in the bucket when you look at your entire financial picture.

But hey - internet advice is worth exactly what you pay for it.

My mortgage starting out in this place was 9.5% in the 1980's and you had to shop hard or buy it down to get into single digits.

Of course houses were way cheaper and accounts like saving and certificates still paid interested that didn't start at .1% or something. Still though, when I see mortgages at two-something it jolts me.

Of course houses were way cheaper and accounts like saving and certificates still paid interested that didn't start at .1% or something. Still though, when I see mortgages at two-something it jolts me.

If the market was lower I'd be more tempted to leave the mortgage as is and pump as much money as possible into the market. With the market where it is and the trade issues/uncertainty we see right now I would be tempted to put into retirement what you get the match on, then take the sure 2.875% return of paying off your mortgage.

My mortgage starting out in this place was 9.5% in the 1980's and you had to shop hard or buy it down to get into single digits.

Of course houses were way cheaper and accounts like saving and certificates still paid interested that didn't start at .1% or something. Still though, when I see mortgages at two-something it jolts me.

Crazy. Unfortunate you were buying at the peak.

You've also likely already paid most of the interest in your mortgage if you only have 9 years left. Most of what you're paying is principal anyway, so I'd say pump the retirement (or any investment part of your portfolio). But, whatever--you're in a better position than most and do whichever will give you more peace of mind.

That's what I was going to say - Interest payments on mortgages are extremely front loaded.

This is a pretty standard graph:

My brother has been a financial advisor for probably 30 years, now in his late 60's. I know he has always said "Never pay off your mortgage" because statistics prove your money over time will do better if it is invested.

Now, a lot of people are saying we are overdue for a market correction, but you still have 40 years or more of investing ahead of you so the market over that period, based on historical evidence, will rise. Plus this predicted correction is just a guess at this point and will depend quite a bit on the election results in November. So that is an important event to consider that is just over 3 months away. Anyway, there's another 2 cents worth.

Now, a lot of people are saying we are overdue for a market correction, but you still have 40 years or more of investing ahead of you so the market over that period, based on historical evidence, will rise. Plus this predicted correction is just a guess at this point and will depend quite a bit on the election results in November. So that is an important event to consider that is just over 3 months away. Anyway, there's another 2 cents worth.

Jacktronic

MONDAYTUESDAYWEDNESDAYTHURSDAYFRIDAYSATURDAYSUNDAY

Just to be clear, I was thinking about lowering the amount that I was putting in my 401k not my Roth 401k. My employer matches 6% on either as long as you do 6%.

It sounds like you're almost at the point where you need to think about whether you want to work until 59.5 or get out early. If you keep plowing into the 401k, you'll no doubt beat the returns of the house on a strictly net worth number. However, if you want to get out of the 9-5 earlier, having your house paid, non retirement investment accounts, or income producing real estate are absolute musts for you. It seems to me like you're crushing it on the 401k/Roth fronts, so you want to get more into your bridge accounts.

If it were me:

1. House paid off (I don't want to pay my mortgage anymore)

2. Max our all retirement accounts

3. Roll Pretax Retirements into Posttax Roth Accounts

4. Taxable Accounts/Real Estate/Annuities/Etc.

5. G-650

Quick question guys, I'm 34 and currently have 15x annual salary saved. Mortgage is paid off and I'm trying to decide whether to blow my monthly net income on bad options plays or cocaine and hookers. Please advise.

Jk, good on you OP, sounds like you are in a great spot.

Just buy your coke in 1/4 ounce increments. Sell a ball in gram and 1/2 gram increments and keep the other ball for yourself. Free or d

It sounds like you're almost at the point where you need to think about whether you want to work until 59.5 or get out early. If you keep plowing into the 401k, you'll no doubt beat the returns of the house on a strictly net worth number. However, if you want to get out of the 9-5 earlier, having your house paid, non retirement investment accounts, or income producing real estate are absolute musts for you. It seems to me like you're crushing it on the 401k/Roth fronts, so you want to get more into your bridge accounts.

If it were me:

1. House paid off (I don't want to pay my mortgage anymore)

2. Max our all retirement accounts

3. Roll Pretax Retirements into Posttax Roth Accounts

4. Taxable Accounts/Real Estate/Annuities/Etc.

5. G-650

Dude he works at pfg. Going to work there is better than being a retiree for 95% of retirees in this country.

Guess you brother does not put a value on peace of mind, or consider risk.My brother has been a financial advisor for probably 30 years, now in his late 60's. I know he has always said "Never pay off your mortgage" because statistics prove your money over time will do better if it is invested.